Argentina's Lithium Landscape: Projects, Potential, and the Path to Battery Production

From Salars to Solutions: How Argentina is Tapping its 'White Gold' to Fuel Tomorrow's Batteries.

1. Argentina's Abundant Natural Resources: A Legacy and a Future

When it comes to natural resources, Argentina is an economic powerhouse, a truth vividly reflected in the early decades of the 20th century. Strolling through Buenos Aires, one might glimpse monuments like the very first Harrods store ever established outside of London (and only1 one excluding airport stores), a tangible link to more glamorous, resource-fueled times. While that era might be a distant memory, I remain bullish on Argentina's natural resources outlook.

Beyond the globally renowned delights of Argentine steak and wines, and the vast soya fields feeding the world's vegetarians, the country is witnessing a significant resurgence in its energy sector. Gas and oil production from its immense Vaca Muerta shale play is rapidly ramping up, with critical infrastructure projects being sanctioned to expedite the monetization of these hydrocarbons23. Just recently, the project pipeline for copper, gold, and silver mining in San Juan province also caught my attention4, signaling a diversified mining boom across the nation.

2. The Lithium Sector: Argentina's Strategic Position in the Energy Transition

Next on my list, and perhaps the most electrifying, is lithium mining – the crucial upstream element for battery production. Argentina holds a pivotal position as a key member of the "Lithium Triangle" in the North-West, a region it shares with neighboring Chile and Bolivia. On the Chilean side, the dominant lithium miners are SQM5 and Albermarle6. Additionally Chile’s copper miner Codelco7 has entered the lithium business, and foreign players such as mining giant Rio Tinto8 are growing their global lithium portfolio, with significant interests in Argentina. Other entrants are junior explorer such as Lithium Chile9 or BYD/Tsingshan10. On the Bolivian side, it’s more state-driven by Yacimientos de Litio Bolivianos (YLB)11, which has set up joint ventures with various foreign companies.

My first trips to Argentina saw me visiting the vast, shimmering salt flats of Salinas Grandes in the provinces of Salta, Catamarca, and Jujuy, a stark reminder of the immense, untapped potential beneath the surface.

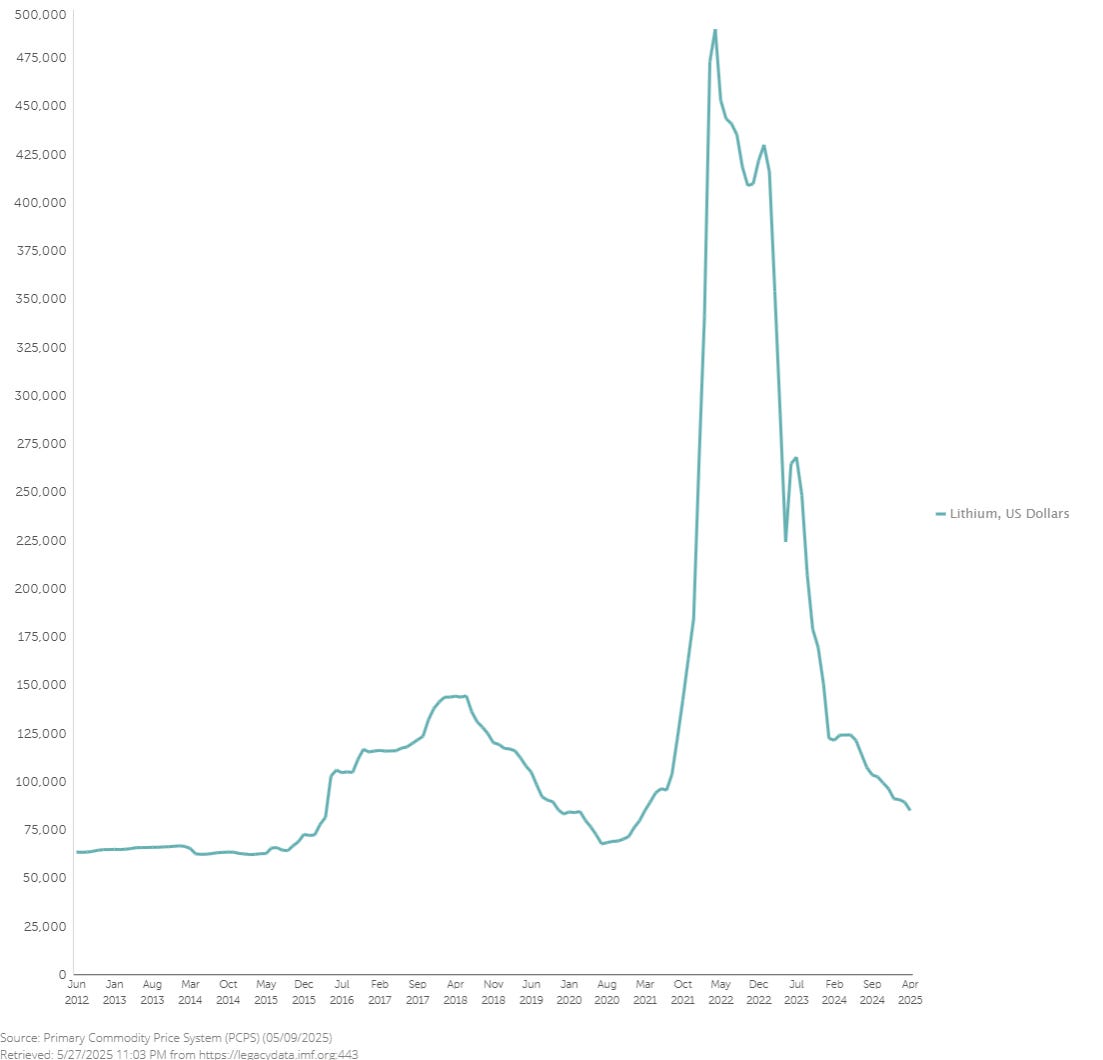

While current lithium prices have seen a dip from their peaks, leading some to question the market's immediate trajectory, the long-term outlook for this critical metal remains undeniably bright. The International Energy Agency (IEA)12 consistently highlights lithium's indispensable role in global energy storage, crucial for the ongoing energy transition and the accelerating electrification of the world - no matter whether it’s your iphone, your EV or utility scale battery energy storage system (BESS). Indeed, the IEA's latest reports continue to forecast robust demand growth for lithium13, despite recent supply additions outweighting with demand increase in the short term. New lithium production is coming online significantly from Argentina and Zimbabwe or maybe Namibia. This long-term conviction is underscored by industry giants like Rio Tinto, who project demand more than doubling from approximately 200 kt LCE in 2024 to 455 kt LCE by 2030, reinforcing their bullish perspective on lithium's future.

3. Why Argentina is an Attractive Lithium Hub: Beyond Geopolitics

Apart from the compelling macroeconomic drivers for lithium, several factors make Argentina particularly attractive for investment:

Geological Endowment: Argentina boasts vast, high-quality lithium brine deposits, particularly within the Lithium Triangle, which are among the largest in the world.

Favorable Regulatory and Fiscal Regimes: The current government has made significant strides in creating an investor-friendly environment. The Régimen de Incentivo a las Grandes Inversiones (RIGI), a landmark incentive scheme, is a game-changer. This regime offers:

30-year fiscal stability, providing crucial predictability for long-term investments.

A competitive corporate income tax rate at 25%.

Accelerated depreciation.

Exemption from import duties, and importantly, benefits related to foreign exchange access and export duties.

Out of 13 projects that have applied for RIGI, a significant portion are lithium initiatives, underscoring the sector's strategic importance to the government.

4. Key Lithium Projects in Argentina: A Glimpse into the Pipeline

Argentina's lithium pipeline is robust, and a visual overview is provided by Argentina’s Geological Mining Agency SegemAR14. Weveral projects at various stages of development moving towards production:

Hombre Muerto Oeste (HMW): 100% owned by Galan Lithium, this project in Catamarca is rapidly progressing. Galan Lithium has applied for RIGI benefits for its Phase 2 expansion. Phase 1 is currently under construction with operations aiming to commence by the first half of 2025, targeting 5.4 ktpa LCE (Lithium Carbonate Equivalent) of lithium chloride concentrate.

Further Information: Galan Lithium Projects

Sal de Oro: 100% owned by POSCO, this project spans the border of Salta and Catamarca. Phase 1, a 25,000 tpa lithium hydroxide plant, commenced operations in October 2024. Phase 2, which includes a 23,000 tpa lithium carbonate plant, has been postponed to Q1 2026 to align with market conditions. POSCO has also applied for RIGI for Sal de Oro.

Further Information: POSCO Newsroom

Rincón: 100% owned by Rio Tinto, located in Salta. This project achieved a significant milestone with its RIGI approval received on May 20, 2025, making it the first mining initiative to be approved under the new regime. A starter plant with 3,000 tpa capacity has reached substantial completion, with the expansion project (to 60,000 tpa of battery-grade lithium carbonate) scheduled to begin construction in mid-2025, with full production expected by 2028.

Further Information: Rio Tinto Rincon

Mariana: Owned by Ganfeng Lithium, located in Salta. The first phase, with an annual production capacity of 20,000 tons of lithium chloride, officially commenced production on February 12, 2025. Ganfeng is also reportedly preparing RIGI applications for the expansion of its salars in Argentina, including Mariana.

Further Information: Ganfeng Lithium (Check for direct Mariana project page within)

Sal de Vida: 100% owned by Rio Tinto (acquired from Allkem/Arcadium Lithium, though your note states Rio Tinto acquired this project directly), located in Catamarca. Project work is progressing with planned first production of 15 ktpa LCE of lithium carbonate in 2027. Rio Tinto expects to soon obtain RIGI benefits for this project.

Further Information: Rio Tinto News

Other Noteworthy Projects: Projects like Cauchari-Olaroz (Lithium Argentina AG and Ganfeng Lithium, already in production) and Centenario-Ratones (Eramet, in production) continue to bolster Argentina's output. Emerging projects like those by NOA Lithium Brines Inc. (Rio Grande, Arizaro, Salinas Grandes) are also advancing through exploration and development stages. Lilac Solutions is piloting Direct Lithium Extraction (DLE) technologies in Jujuy, indicating a push towards more advanced extraction methods.

5. How Lithium is Mined: From Brine to Battery

The extraction of lithium primarily depends on its geological source. In Argentina, the dominant method is brine extraction, utilizing the vast salt flats (salars). However, advanced techniques like Direct Lithium Extraction (DLE) are gaining traction.

Brine Extraction (from Salars/Salt Flats):

Initial Product: After solar evaporation in large, shallow ponds, the primary output is a concentrated lithium chloride (LiCl) brine. This is a liquid solution with a higher concentration of lithium salts.

Final Products: This concentrated brine then undergoes chemical processing to produce:

Lithium Carbonate (Li2CO3): This is the most common primary product from brines, achieved by adding soda ash (Na2CO3) to precipitate Li2CO3.

Lithium Hydroxide (LiOH⋅H2O): While less common as a direct primary product from brines, lithium carbonate can be further processed (converted) into lithium hydroxide. This conversion involves additional chemical steps and energy.

Hard Rock Mining (from Spodumene):

This method involves extracting lithium from hard rock deposits containing lithium-bearing minerals, primarily spodumene. This is the dominant mining method in countries like Australia, which is the world's largest producer of hard rock lithium, as well as in China, Canada, and parts of Europe.

Initial Product: The direct output after mining, crushing, grinding, and flotation is spodumene concentrate. This is a solid mineral ore, typically containing around 6% Li2O.

Final Products: The spodumene concentrate requires extensive chemical processing (roasting, acid leaching, purification) to produce:

Lithium Hydroxide (LiOH⋅H2O): Hard rock operations are often designed to directly produce lithium hydroxide, which is increasingly favored for high-nickel content cathodes in electric vehicle (EV) batteries due to its higher energy density.

Lithium Carbonate (Li2CO3): Spodumene can also be processed to produce lithium carbonate, though it may then be converted to hydroxide if required for specific battery chemistries.

Clay Extraction (Emerging Technology):

Initial Product: After mining and chemical leaching, the initial product is a lithium-bearing leachate. This is a solution containing dissolved lithium along with various impurities from the clay.

Final Products: This leachate would require significant purification and chemical conversion to produce:

Lithium Carbonate (Li2CO3)

Lithium Hydroxide (LiOH⋅H2O)

Direct Lithium Extraction (DLE):

Initial Product: DLE technologies directly produce a highly concentrated and purified lithium chloride (LiCl) solution from the brine, bypassing the need for large evaporation ponds.

Final Products: This concentrated LiCl solution is then processed to produce:

Lithium Carbonate (Li2CO3)

Lithium Hydroxide (LiOH⋅H2O)

While Argentina primarily utilizes traditional brine extraction, the presence of DLE pilot projects, such as Lilac's initiatives15, clearly signals a future shift towards more environmentally efficient methods. This focus on DLE is part of a broader global trend, with companies like Vulcan Energy in Germany16 notably piloting the technology to extract lithium from geothermal brines, demonstrating its versatility and potential beyond traditional salars.

Each mining method comes with a distinct cost profile. Historically, traditional brine evaporation has been considered the lowest-cost method for lithium production, largely due to its reliance on solar energy and simpler initial infrastructure. Hard rock mining, while offering faster processing once the mine is operational, generally incurs higher capital and operating expenditures due to the intensive mining and processing requirements (e.g., crushing, grinding, roasting). Emerging technologies like DLE and clay extraction often involve higher initial capital investments for specialized plants but promise lower operating costs, faster production, and reduced environmental footprints, making them increasingly competitive as the technology matures. The overall cost efficiency of a project is crucial in determining its viability, especially amidst fluctuating market prices.

6. The Refined Products: What Batteries Really Need

After the initial mining or extraction of lithium, significant additional refining is absolutely essential to produce materials suitable for batteries. The raw materials are never pure enough for direct use. The goal for all lithium mining operations is to produce high-purity, battery-grade lithium carbonate or lithium hydroxide, which are the primary forms utilized by battery manufacturers.

Lithium Carbonate (Li2CO3): This compound is widely used in LFP (lithium iron phosphate) battery cathodes, which are known for their safety and cost-effectiveness, and also in some NMC (nickel-manganese-cobalt) battery chemistries. It also has applications beyond batteries, in ceramics, glass, and pharmaceuticals.

Lithium Hydroxide (LiOH⋅H2O): This is increasingly preferred for high-nickel content NMC and NCA (nickel-cobalt-aluminum) cathodes. These cathodes offer higher energy density, making them ideal for longer-range electric vehicles. Producing hydroxide from carbonate involves an additional conversion step and cost, but its advantages in battery performance are driving this demand. The trend in battery technology is indeed seeing a shift towards higher-nickel NMC chemistries requiring lithium hydroxide, while LFP batteries, using lithium carbonate, remain popular for their cost-effectiveness and safety in other EV segments and energy storage.

7. Evolving Battery Landscape: The Enduring Need for Lithium

The battery market is indeed dynamic, with ongoing discussions about the shift in demand between different chemistries. While there's a notable trend towards LFP batteries for certain applications, particularly in mass-market electric vehicles and stationary energy storage, it's crucial to understand that this does not diminish the overall need for lithium.

LFP batteries still require lithium carbonate. The shift towards LFP simply changes the preferred lithium compound, not the fundamental need for lithium itself.

NMC batteries, which typically use lithium hydroxide, continue to be essential for high-performance, long-range EVs where energy density is paramount.

Beyond LFP and NMC, other emerging battery technologies like solid-state batteries, which are seen as the next frontier for higher energy density and safety, are also lithium-ion based and will require significant amounts of lithium. Sodium-ion batteries are an alternative for specific use cases but are not expected to fully displace lithium-ion in all major applications.

Therefore, regardless of the evolving cathode chemistry mix, lithium remains an indispensable and irreplaceable component for the vast majority of current and next-generation battery technologies powering our electrified future. The global demand for lithium, whether as carbonate or hydroxide, is set to continue its strong growth trajectory.

Conclusion: Argentina's White Gold on the Global Stage

All in all, Argentina's lithium sector truly appears to be its 'white gold.' With immense natural endowments, a supportive regulatory environment, and a robust project pipeline, the nation is solidifying its position as a critical player in the global energy transition. As the world accelerates its move towards electrification and sustainable energy solutions, Argentina's contribution of refined lithium products will be indispensable for all major battery chemistries, cementing its role as a powerhouse in the new energy economy. While the recent volatility in lithium prices (as seen in the accompanying chart) presents short-term headwinds, the underlying long-term demand for this crucial metal suggests a promising trajectory for Argentina's 'white gold.

The parable of Argentina. The Economist. (Feb 15, 2014) https://www.economist.com/leaders/2014/02/15/the-parable-of-argentina

$13.7 billion deals for $50B South American LNG project put into Bermuda firm’s hands. https://www.offshore-energy.biz/13-7-billion-deals-for-50b-south-american-lng-project-put-into-bermuda-firms-hands/

Argentina LNG. https://argentina-lng.ypf.com/en/

From Vine to Vein: San Juan's Mineral Wealth

San Juan, nestled in the shadow of Argentina's famed wine region, Mendoza, offers more than just robust red Malbecs. While Mendoza has recently captured attention for its mining prospects and development – as highlighted in the Financial Times article "Argentina's wine heartland eyes copper riches"

SQM Homepage: https://sqm.com/en/productos/litio-y-derivados/

Albermarle Homepage: https://www.albemarle.com/us/en/global-locations/chile